Welcome to our ultimate guide to investment risk. Like our other ultimate guides, this article will cover as much breadth and depth as you’ll need as a beginner to master the concept of investment risk. Risk is easily the most important concept to master as a new investor. In fact, you shouldn’t invest a single pound until you’ve read a guide to risk such as this and feel comfortable with all of the topics within.

Ultimate guide to investment risk contents:

- Definition of risk

- How to approach risk

- A necessary evil

- Remaining at the table

- Types of risk and how we mitigate

- Investment risk

- Alpha risk

- Beta risk

- Liquidity risk

- Inflation risk

- Counterparty risk

- Cycle risk

- Tax policy risk

- Fraud risk

- Investment risk

- The efficient frontier: optimising for risk in a portfolio

- Efficient frontier concept

- Asset classes

- Risk-adjusted returns

- Why high returns don’t always justify the means

- The Sharpe ratio

- Risk and age

- Glitches in the risk v return matrix

- 100% guaranteed cash savings accounts

- Pension contributions matching by employers

- How to manage the stress of risk

- Think about the long-term

- The income mindset

Definition of risk

Risk is the chance that something will go wrong. A riskier investment is one that has a higher likelihood of a poor outcome, or has a wider range of possible outcomes, making it difficult to accurately predict what will happen.

In the stock market, risk can manifest as volatile share price swings, cuts to dividends and even the total loss in value of an investment.

How to approach risk

In this first section of our ultimate guide to investment risk, we’ll look at risk from a few helpful angles to nudge your mindset before we get into the detail of what risks investors will be exposed to.

A necessary evil

Risk is an enemy of investors, but one that investors cannot avoid completely. Investors have a love-hate relationship with risk because the negative qualities of risk actually enable good returns from investments in the first place.

You will hear many times in this article that risk and returns are correlated, which means that when risk is higher, returns to investors also tend to be higher. This relationship isn’t coincidental.

The presence of risk causes high investment returns.

Consider the following example to be enlighted as to why risk is so fundamental to the equation of expected returns.

Illustration A: Lucy asks investor Hayley to provide her new company with an equity investment to buy stock and pay for the lease on the store. Hayley understands Lucy’s venture to be high risk because she is inexperienced, and is aware that a similar shop has recently closed down on the same street due to poor sales.

Hayley, therefore, asks for a larger share of the business in return for her initial investment. Lucy must accept, as she cannot solicit a better offer after speaking with other concerned investors.

The higher stake that Hayley would receive as part of the deal serves to increase the possible upside of the investment if the shop becomes a success, as Hayley will now receive a greater share of the unit’s profits if they materialise.

In summary:

When the risk is high, for the same expected outcome, investors will expect to pay less to invest in an opportunity. Or for the same initial investment; investors will expect to be offered a greater share of the potential reward.

If investment prices are not discounted to reflect risk, then investors will choose to invest their funds elsewhere for less risk, and the fund-raising will not be successful.

For this reason, risky ventures would not successfully raise finance from investors without offering those investors a proportionate discount to entice them to accept a riskier outcome.

Although we’ve focused on a small business owner & angel investor scenario, the same dynamic is in play when shares are traded between investors on the stock market. All else being equal, the shares of a risky company will trade at a lower price than a firm with a very certain trajectory.

Risk is therefore a key driver of pricing, and the price at which you invest in an asset is naturally a very important component of the financial return you could enjoy from an investment portfolio.

Remaining at the table

Next, we’ll use a poker analogy to explain why managing risk isn’t quite as dull as it sounds.

You might think that picking stocks to invest in is somewhat similar to playing a hand of poker.

In a game of Texas Hold’em you don’t know all the facts when you stake cash on your hand, but with some skill (and luck), a strong hand should produce a financial reward.

We believe that a better analogy for investing is playing an entire tournament of poker. That’s because, just like in a poker tournament – your outcome isn’t determined by a single hand, but rather a long series of hands played in succession.

To win a poker tournament, by definition you’ll need to beat your opponent with a winning hand. But to actually get to the final table, and the ultimate showdown, you need more than just a single stroke of luck:

You need to have survived this far.

Wins and losses sound like polar opposites, but when they’re applied to investing, they’re not totally symmetrical concepts.

Here are some clear differences:

- When buying shares, your maximum loss is limited to the amount you deposited. However, your maximum gain is unlimited because there is no upper limit to the theoretical value of a company or its shares.

- If you lose 50% of your starting capital, you need to experience a 100% gain to get back to where you started.

- When making a series of high-stakes investments, if you strike it rich, there is still a chance of losing all of your money on the next investment you buy. But if you are wiped out, you cannot make any further investments, so the loss is guaranteed.

Side note: this concept is known as ‘gamblers ruin’. It has nothing to do with the ‘house edge’ on odds, yet it accounts for a not insignificant proportion of losers in casinos and bookmakers.

These fundamental differences between profits and losses provide a hint at why risk is treated so seriously by investment professionals. Gains and losses aren’t simply opposite sides of the same coin. Losses (particularly those incurred early in an investment time period) can have a disproportionate effect on total investment returns even if an investor later enjoys healthy returns.

Types of risk

In this main part of our investment risk guide, we’ll break down the word ‘risk’ into specific examples of ‘what can go wrong’ while investing.

- Investment risk

- Alpha risk

- Beta risk

- Liquidity risk

- Inflation risk

- Counterparty risk

- Cycle risk

- Tax policy risk

Investment risk

Investment risk is the straightforward risk that the capital value or income of your investment is worse than you expected.

When the stock market is generally described as a ‘risky investment’, this is likely what the commentator is referring to.

When you place money in a government-backed savings account, you can predict to the penny how much that account will be worth in one week’s time.

In contrast, a new shareholder in a company can only hope that the value of their holdings will rise in value over that period. They could fall by 5%, or even rise by 5%. This is completely unknown as the shareholder looks into the future.

Investment risk is handily split into two elements to help us understand what drives the daily up and downs in the price of a share or other public investment. Those elements are Alpha and Beta.

Alpha risk, also known as ‘specific risk’, relates to new information or events that specifically impact your investment. If you invest in a theatre company, its venue could be demolished by fire the following evening. This is a specific risk. Risk isn’t biased towards the negative – the theatre could beat all expectations with a series of 5-star reviews on an opening night and send its share price soaring. Either way, these types of events contribute to volatility and volatility = risk.

Beta risk, sometimes called ‘market risk’ is driven by macro-economic or other political events that cascade across nations and economies, resulting in optimism or pessimism that affects most shares. If a country slides into recession, the gloomy outlook will likely weigh heavily on the prices of many sectors.

Liquidity risk

Liquidity is a measure of how quickly you can turn a paper investment into spendable cash in your hands (at a fair price).

It’s a major constraint on many savers and investors because different types of investments have dramatically different levels of liquidity. Many savers are not prepared to be separated from their money for an extended period of time and are prevented from accessing it during an emergency. Therefore liquidity risk should play a big role when you select which asset classes are suitable for your portfolio.

While investment risk tests your ability to withstand price shocks, liquidity risk tests your ability to be unable to access your investment for a long period of time.

Liquidity ranking of investments

Here’s a very simplistic guide to how liquid different types of investments are, ranking investments from most to least liquid:

- Gold bullion bars or coins: same day

- Instant access cash savings account: 1-2 working days

- Publicly traded equities held in a stockbroker account: 2 working days

- Exchange-traded funds: 2 working days

- Private mutual funds such as unit trusts and OEIC funds: 2 – 5 working days

- Private property investment, such as a buy-to-let property: 6-9 months

- Fixed term savings account (1 year): 1 year

- Hedge funds: 2+ years

- Venture capital trust investment: 2+ years

- Private shareholding in a small to medium-sized business: 6 months to 3 years

- Fixed term savings account (3 years): 3 years

Fickle liquidity during adverse market conditions

Liquidity is a tricky risk to measure because it fluctuates with the cycle of the financial markets.

During the good times, when there are many buyers for an asset and prices are rising, it will be much easier to sell your holdings for a good price in a short space of time.

It can be easy to be lulled into a false sense of security as virtually all investments feel very liquid during bull markets.

Remember that liquidity is only put to the test when you personally want to sell. It’s much more likely that you will be trying to sell during a downturn than during a bull market.

You should rate the liquidity of an investment by a reasonably possible worst-case performance. How liquid would it be during a significant recession, for example?

You can model the liquidity of an asset by answering the question: who is providing the liquidity?

Liquidity generally comes in three forms:

Public market – you can freely sell assets to any willing buyer on the market, e.g. stocks & shares, or gold bullion which you can sell to any jewellery merchant or private individual.

Private market – you can request to sell assets, however, the administrator may be able to control which sell requests are settled in which order (for example they may enforce a queueing system for withdrawals).

Private provider – you may only cash out if the provider is willing to reimburse you, for example, a bank or fund manager. They may have total discretion as to whether to honour your request during adverse market conditions if high volumes of selling would further depress asset prices and discriminate against other unit holders in the fund. For example, during a run on a bank or massive withdrawals from an equity fund.

In general, public markets provide the greatest levels of liquidity because in theory there will always be a buyer for an asset at the right price. During volatile trading sessions, that price may be lower if buyers become nervous, but this is nevertheless an offer to cash-out your investment.

Investors should be very sceptical of the liquidity of private marketplaces. These include peer-to-peer trading of property, P2P loans and other private equity investments. The providers of these marketplaces will be quick to highlight that such features offer exit options but are not a guarantee of liquidity.

For example, PropertyPartner.co, a leading provider of crowdfunded property investments in the UK includes the following wording in its disclaimer: “5 yearly exit protection or exit on platform subject to price & demand.” This is a reminder to investors that any offers of early exits via their resale marketplace are not guaranteed as it relies upon matching demand from buyers to fulfil sellers wishes.

Real examples of liquidity risks

If you’d like to read about some real-life examples of liquidity issues, take your pick:

Investors were trapped in the Woodford Equity Income Fund when withdrawals were suspend in 2017. Neil Woodford was a ‘star’ fund manager with an excellent track record, which unravelled after his mainstream equity fund made a series of risky bets on unlisted (and thus unliquid) assets which subsequently lost value. As dissatisfied investors began to withdraw, the fund realised it didn’t have sufficient liquidity to fulfil these requests, forcing it to dispose of holdings in a fire sale, resulting in further losses. The fund eventually suspended withdrawals to protect investors by providing it with the breathing room to make orderly sales and receive the maximum value for its holdings as it offloaded them.

Investors faced a several-month wait to withdraw funds from peer-to-peer lending platforms such as Assetz Capital at the onset of the covid-19 pandemic. Although these platforms may look and feel like a bank, particularly with their ‘30-day access’ accounts, they are in fact a marketplace and access is not guaranteed in their terms & conditions. Assetz Capital also introduced a 1% charge on withdrawals during this period; a measure designed to reduce appetite for sales. When the economy eventually recovered, demand for business loans from new investors was so intense that restrictions were actually placed the opposite way around to slow the flow of capital into the platform as buyer interest was outstripping the volume of loans available to fund on the platform. Both of these events are a feature of any platform with finite liquidity and should not come as a surprise to investors. This is a simple limitation of a secondary marketplace with relatively low trading volume. Assetz Capital has done a good job in managing investor expectations during these challenging times.

Liquidity risk is often attached to the platform or collective investment fund rather than the underlying assets.

It is worth briefly noting that investors should differentiate between the liquidity of the underlying assets of a fund/investment and the liquidity of the actual investment held by the individual.

For example, property Real Estate Investment Trusts (REITs) such as LandSec PLC invest in long-term property development projects that are extremely illiquid and only produce cash returns after 3 – 6 years. However, direct investment in LandSec PLC takes the form of publicly traded shares which can be sold within two working days via your stocks & shares ISA.

In contrast, a retiree may have invested in a ‘with-profits’ investment funds provider such as Legal & General, Aviva or Aegon. This investment may too have invested in LandSec PLC, but the actual investment held by the pensioner is some units in the fund itself. These may come with a longer time period for sale and penalties for withdrawals and therefore have higher liquidity risk.

Inflation risk

No risk in this article is more topical than the risk of inflation.

Inflation (see definition) is the rate of increase in prices across an economy. When prices rise higher, consumers can buy fewer products & services with the same pot of money. It follows that high inflation is bad news for consumers and investors alike. Inflation is the enemy of living standards.

Inflation risk doesn’t apply differently to each investment you choose. Instead, it is better to visualise inflation as a rising tide that eats away at the value of all of the cash and monetary assets you may hold.

Investors cannot truly ‘escape’ inflation, only seeking to ‘beat’ it by producing a monetary return from their portfolio that exceeds the rate of inflation. This way, they may still enjoy a real increase in spending power, despite its corrosive effect.

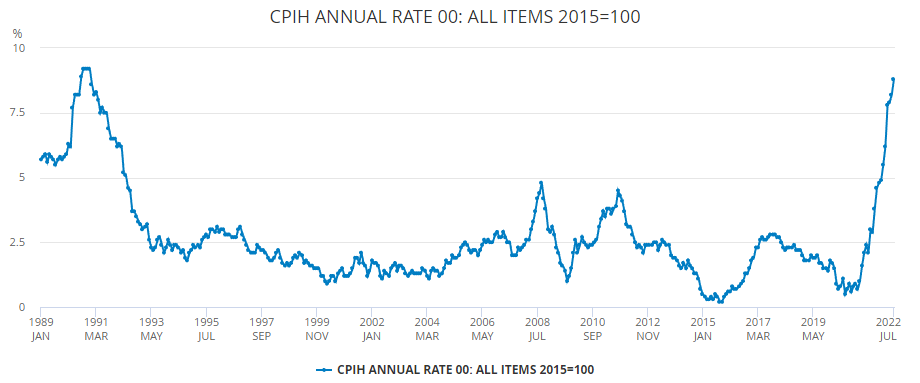

Historical rates of inflation

This chart, compiled by the Office for National Statistics is the official record of inflation.

You can see that over the last two decades, inflation has averaged around 2% – 3%, which is close to the Bank of England’s 2% target.

Since 2021, the rate of inflation has skyrocketed owing to several factors including supply shortages, low rates of unemployment and an energy crisis following Russia’s invasion of Ukraine.

How does inflation risk affect investor decision-making?

Inflation risk has a curious effect on investors – it actually encourages them to take on more investment risk.

That’s because low-risk or no-risk investments usually fail to beat the inflation rate. Take a look at any instant access savings account interest rate over the last few years and compare it to the chart above. It is unlikely a bank has offered a rate of return that actually exceeded the inflation rate.

This is no coincidence. Interest rates tend to roughly track changes in inflation because interest rates are the main tool at the disposal of the Bank of England to keep inflation under control. When inflation is low, the BoE will reduce interest rates to stimulate consumer spending and add upward pressure to prices. When inflation is too high, the BoE will increase interest rates to encourage saving and sap consumers of their spending power through higher mortgage loan repayments. Because of this relationship, the interest available on bank accounts will be similar to (and often less than) the rate of inflation.

If a bank account won’t grow fast enough to even maintain its spending power – what is the point of using one? This is the question that prompts investors to take on investment risk and raise their returns. Only by beating the rate of inflation will investors actually be able to grow the real value of their wealth and meet ambitious financial goals.

For more ideas of How to protect your investments from inflation, read our article.

Counterparty risk

When you invest, you place your faith in the brokers, intermediaries, advisors and fund managers that will handle your money.

In many cases, your money only ‘passes through’ these third parties and therefore you are not highly exposed to the failure of their business, however, sometimes the value of an investment is completely dependent on the counterparty remaining solvent.

Examples of these include:

Bank accounts: When you deposit money into a bank account, you are expressly relying upon the solvency of the bank to honour your deposit when you come to make a withdrawal.

Corporate bonds: A bond is an ‘IOU’ from a government or company, received in exchange for advancing that organisation a lump sum of cash. The bond issuer will only be able to continue making repayments of principal and interest if they remain solvent and able to pay. When a firm collapses, bondholders are among the many creditors that may only receive pennies in the pound on their claims on the firms’ assets.

Structured products: Investment schemes that offer fixed returns if certain scenarios (such as the performance of an equity index) are met. These returns are underwritten by a financial institution such as an investment bank, and therefore you are reliant upon that firm remaining solvent to be able to pay out any proceeds at the maturity date.

How to reduce (or eliminate) counterparty risk

Let’s start with the most important source of counterparty risk: banks. In 2022, approximately £3.5 trillion pounds is held on deposit with a UK bank. That’s a lot of money that UK savers dearly hope they will see once again.

The UK financial services regulators created a useful scheme in 2001 called the Financial Services Compensation Scheme. In the event that a bank collapses, this scheme promises to repay savers any lost savings up to the value of £85,000 per banking group.

£85,000 isn’t a huge allowance when you consider that many pensioners have hundreds of thousands of pounds locked away in savings accounts. To maximise available protection, wealthy savers must spread their cash across different banking groups to receive £85,000 of protection.

This apparently miserly limit is quite wise because it nudges the British population to not put all of their money in one basket, ensuring that no single bank becomes dominant and ‘too big to fail’.

The FSCS scheme was put to the test in 2008/2009 when it jumped into action to reimburse savers in the collapsed Icelandic banks Kaupthing & Landsbanki which had attracted £ billions in deposits prior to the Great Recession. Savers needed to wait a few months for reimbursement but it was generally accepted that the payouts were handled properly and the existence of the FSCS helped to prevent a further run on British banks during the crisis.

Non-deposit assets, like bonds and structured products, are not covered by the FSCS and therefore investments are made at the buyer’s risk.

It’s therefore advisable to conduct due diligence on the counterparty you may rely upon for your future investment returns.

If you are financially literate, you may wish to analyse their most recently published financial statements. Alternatively, you could ask for the advice of a qualified financial adviser who will be able to warn you of excessive counterparty risk.

Counterparty failures are not limited to Icelandic banks. In 2008, the collapse of the US investment bank Lehman Brothers caused grave concern to many UK investors, because Lehman was a counterparty to structured products, backing at least 1% of all products in the market at the time. Investors received approximately 42p for every £1 that Lehman Brothers owed; which will have been viewed as a catastrophic loss for some.

Cycle risk

When one steps back and looks at the eb and flow of the economy and the financial markets that sit atop them, it becomes clear that they follow cycles of boom and bust.

The economic cycle, also known as the business cycle, is measured by the expansion and contraction of the value of goods and services produced by an economy, known as Gross Domestic Product (GDP). The good years are said to experience ‘economic growth’, and the bad years – where the economy actually shrinks in size – are called a recession.

The financial markets cycle is visible through the rise and fall in the value (also known as market capitalisation) of publicly traded assets, such as the stock market and bond markets. These can be seen by looking at the price of the FTSE 100 index since inception.

Cycles present a risk to investors because they add a layer of unpredictability into the mix. The peak or trough of cycles cannot easily be predicted, because they occur with different frequencies and different lengths.

The economic cycle results in record profits, followed by many companies actually incurring losses. In anticipation of this cycle, the financial markets cycle reaches a peak ahead of the real economy, and will experience sharp drawbacks in value when an economic recession appears on the cards in the medium term.

If an investor places money into the stock market at the peak and holds it for the medium term, they may still have a disappointing experience if they are fully invested during a stock market crash.

How to manage cycle risk

The financial markets cycle tends to lift and crush the valuation of all assets across the board, meaning that savvy stock-picking does not hold the answer to this problem.

Investors will always ask the question, is now a good time to invest in the stock market? The question opens the possibility that financial experts can simply provide a yes or no answer. In truth, no-one can reliably inform you whether you should buy shares now, nor when later you should sell them

The latest stock market outlook is always technically neutral, because prices adjust to the point that investors feel best reflects the risks and rewards of the future. This means there is no perfect time to buy shares.

The consensus is that investors should simply invest gradually throughout their whole life, such that some investments will be perfectly timed, and others disastrously, but overall the average purchase timing relative to a boom or bust will typical, and not extremely lucky or unlucky.

Tax policy risk

Speaking from a UK perspective, the way investments are taxed is quite favourable for most retail investors.

The advent of the Stocks & Shares ISA has allowed middle-income families to build up healthy pots of investments with no taxes to pay on dividend income or capital gains.

The rate of personal income tax on dividends is also less than the equivalent taxes on employment income, particularly when social security is also brought into the equation.

That being said, a risk arises that future governments may change tax policy in such a way that an investor is significantly worse off, and may even come to regret their investment decisions.

How to address tax policy risk

The practical way to neutralise tax policy risk is to build a portfolio that makes sense regardless of tax rules. In particularly, you could avoid making investments that rely upon aggressive tax interpretations or hinge upon a new tax break (as new tax rules have the greatest chance of being temporary).

You could also tailor your tax planning towards solutions that deliver tax relief upfront, rather than at a future date.

For example, private pension schemes provide tax-relief at the point of depositing into the pension, either through a salary sacrifice scheme saving you tax in the same month, or through a tax return filing that allows you to claim back tax for pension contributions in hindsight.

Once tax relief has been given, the pension pot is taxable going forwards as current rules treat drawdowns from pension pots as subject to income tax.

This has relatively low tax policy risk because you’ve already been handed the tax relief in the form of extra cash, and we already expect to be taxed on drawdowns in the future. For the government to u-turn on this policy and remove money from pension pots would be very difficult politically speaking, as would taxing ordinary pension income at a higher rate than any other income.

In contrast, a scheme that relies upon tax relief given in the future, like the rollover/holdover rules on reinvesting gains from equity investments in private companies could be withdrawn at any time, leaving some scratching their heads as to whether in hindsight they wish they hadn’t invested in small risky businesses in the first place.

Even the best tax books make abundantly clear that the rules of tax are complex and always subject to change. When financial planning, tax should only ever be a secondary factor and never the primary driver behind a particular investment strategy or product.

Investment fraud risk

Investment fraud risk is the risk that you may lose hard earned money as the victim of an investment scam.

This could take several forms:

- You are encourage to buy shares in a penny stock or buy a niche cryptocurrency that is overvalued and subsequently loses money (‘Pump & dump scam).

- You invest with a firm that does not use the money as its stated purpose and instead the operators flee with the money.

- You invest in a firm that doesn’t create real value, but instead creates the impression of financial success by using funds from next investor to pay returns to old investors (Ponzi scheme).

- You are missold a high-risk investment as a low-risk investment, and subsequently the underlying investment collapses, leaving you with losses on what was sold as a sure bet.

To help you navigate the world of investment scams, we’ve pulled together a comprehensive guide about how to spot investment scams that we won’t reiterate in this article because it’s such a detailed topic. Visit that article to read more.

The efficient frontier: optimising for risk in a portfolio

Academics have published countless papers since the 1920’s that attempt to articulate the best process for building a portfolio to reduce risk and maximises return. Many professors and students have made interesting discoveries that have incrementally informed our view of how portfolios can be used to mitigate risk, and these are lessons that we can apply in our own finances.

In this section we’ll skim the theory in bite-sized chunks to takeaway the core elements that inform modern portfolio management theory.

Bitesize theory 1: investing on the efficient frontier

All investments contain an element of risk and the promise of return, in many different interactions. When so many dimensions exist, it can be difficult to choose the best investment.

For example, which of the following investments is better when their risk and return is scored out of 10:

- 1/10 risk, 4/10 return

- 3/10 risk, 5/10 return

Therefore isn’t an objective answer to this question. Investment B contains much higher risk than Investment A, but it does offer an improved return. Some investors may consider this too modest a risk premium to justify the additional risk, but investors who are simply seeking to enhance their returns may disagree.

However, they should all be able to agree that the following investment is sub-optimal:

- 2/10 risk, 4/10 return

This investment may initially appear attractive because it contains less risk than Investment B, but it offers the same return as Investment A – the lowest risk investment of the group.

When faced with a choice between investment A & C, picking A is the no-brainer because for the same return a lower-risk option is available.

This analogy leads to the conclusion of the efficient frontier hypothesis which is that, for a given level of risk, investors should only invest in the assets that offer the higher return.

Plotted on a chart, each of this highest-return assets for each level of risk show the best possible return available depending on risk preference. Together, they plot a curve that demonstrates how generously the market rewards additional risk. Any investments that sit under this curve (because they offer lower returns than other assets with the same risk) are sub-optimal and should not be purchased, per the theory.

Bitesize theory 2: Asset diversification

Investment risk is quantified by taking the standard deviation of an asset price over time.

In layman terms, the standard deviation of a series of prices is the typical distance a price point is from its long run average. The more wild the price has bounced around, the higher its standard deviation will be. If a price has remained perfectly still for the whole series, its standard deviation will be 0, as the price never deviated from the average.

Standard deviation is a simple statistic that we can calculate from any data series of prices, and it’s a helpful number for academics to ‘solve for’ when looking for the perfect portfolio.

Diversification neutralises alpha risk

When introducing investment risk above, we explained that investment risk is volatility in prices, and that these price movements stem from a combination of specific (alpha) company factors and broad (beta) economic factors.

Both sources of volatility would hurt an investor with equal measure, but something magical happens when multiple assets are combined together in a portfolio.

Broad beta factors will impact most assets, and drive the total portfolio up or down, depending on the nature of the news. However Alpha factors are random, and therefore as more and more companies are included, the positive and negative impacts of Alpha offset one another. The stellar growth announced by one company may offset the disappointing update issued by another.

This makes sense because investors price shares at the best neutral expectation of the future, good news and bad news that moves prices should be fairly equal.

Portfolio managers and statisticians have modelled the standard deviation of portfolios to output the optimal number of assets to hold in a portfolio to bring Alpha risk to as low as possible while not incurring excessive holding & dealing costs.

The answer is 20.

After you have added 20 assets to a portfolio, you will see only tiny incremental reductions in Alpha risk – a poor return on the additional fees you will incur to manage an ever-larger portfolio.

This gives an insight to why most fund managers include over 20 assets in their fund, and why diversification is one of the basic principles that virtually all successful investors adhere to.

Bitesize theory 3: asset classes

Moving beyond the picking of 20 assets to create a portfolio, you could attempt to mute the impact of Beta by investing in different asset classes.

Asset classes are investments with different legal forms, rights, rewards & risks. They have different characteristics as a result.

Shares are one asset class, with other key classes including property, cash and bonds.

While Beta risks may inflate or depress all equities in a similar manner, bonds for example could react in a different way – perhaps even increasing in value in response to the same news that took equity markets downward.

Spreading your wealth across multiple asset classes can undoubtedly reduce the overall volatility of your portfolio, but it will also affect your expected return. Equities are the strongest performing of all assets, therefore the more corporate bonds and cash are introduced into your portfolio, the lower the expected return of your combined portfolio will be.

If you are curious about what asset classes are out there and what characteristics they have, check out our essential guide to the 9 major asset classes.

Risk-adjusted returns

Why great results don’t always justify the means

In the previous section we introduced the concept of the efficient frontier; the idea that for a given level of risk there will only be one asset with the highest expected return.

The question quickly moves onto ‘which level of risk is the correct level?’

As risk increases, expected returns leap higher and higher. But are there diminishing returns, and how high is too high?

Well, one limitation is going to be your own appetite to risk. Take our risk appetite questionnaire for an idea of where your limit might be. If you’ve had a cautious attitude towards money all of your life, don’t expect to suddenly be happy stomaching 4% daily drops in the value of your wealth simply because you’ve become smarter about investing. Risk appetite is partially part of your personality and your brain will tell you quite quickly when it is not comfortable taking the risks you’ve signed up for.

Just because a famous investor achieved a high return doesn’t mean that they followed an approach that you should take. In this particular version of reality – their strategy panned out – but what if their result was just a fluke?

This isn’t just a thought experiment, because if you’re planning to now adopt their investment strategy – you’re about to run a real experiment of your very own. With your own money on the line, it’s well worth considering what risk the celebrity actually took to achieve their results.

For example, we could look at the case of real estate investors who invested in property in 2010 and took out huge mortgages to scale-up a buy-to-let portfolio. Due to the leverage involved, and a benign, upward property market, this strategy paid off after a few years. However, it’s clear that any investor using 75% leverage to buy assets would be wiped out to zero if house prices fell by 25%.

These investors benefitted from once-in-a-lifetime rock-bottom interest rates, plus monetary stimulus and a relatively stable economic environment. If any one these factors was removed from the equation, it could have been very unpleasant for them. Leveraged investors are always the first to hit the dust when an investment cycle comes to an end. Consider the $4bn in losses incurred by leveraged Crypto investors in the first wave of price consolidation at the end of 2021.

What matters is not the absolute return someone achieved – but their return relative to the amount of risk they took.

As a very simple formulae, it could look like this:

Total return / Level of risk = Risk adjusted return.

If you want to do this properly, you should deduct the going risk-free return from the total return (As everyone will earn the risk-free return by default without risking anything). This gives the premium return that was generated as a result of choosing a more risky investment.

Then divide this return premium by the standard deviation of investment returns, i.e. risk.

This effectively outputs how much premium return you are earning for each unit of risk. This is known as the Sharpe Ratio, and is a very common tool used by portfolio managers in assessing whether a strategy was genuinely brilliant, or a lucky punt.

Risk and age

We look at investment risks through different lenses as we grow older.

While living our years, we have personally experienced the highs and lows of risk-taking, we’ve upped the stakes as we’ve built up a savings pot, and as time ticks away we lose our capacity to rebound from financial disaster.

A financially comfortable 25 year old looking to buy shares for £1,000 in the stock market can take an incredible amount of risk.

If they bought a single Chinese company which subsequently went to zero, life would continue. Because they’re earning a salary, they know that they could save that money up again in a matter of weeks or months. It would be an inconvenience and a source of regret, but ultimately it would be a blip in the footnote of their financial future.

A 75 year old is not in the same position when looking to invest their £400,000 pension pot. That po, together with the State Pension is designed to provide them with their entire spending power until the day they leave this earth. It might be generous in size, but it’s terrifyingly finite. Save for a lucky lottery win, that is their lot, and if it disappears in an investment scam, poverty will ensue.

Rather than being a sideeffect of the crankiness or cynical attitude older people tend to embrace, fiscal conservatism is actually a logical survival tactic. When it hits home that you no longer have any capacity to earn extra money, you treat your existing savings like they are precious.

Glitches in the risk v return matrix

Above, we have covered the rock-solid relationship between risk and return. This relationship is theoretical, and some real-life factors actually screw with the formula somewhat.

Where a risk is artificially lowers, or a return is artificially enhanced, you should give serious consideration to pursuing it, because these two opportunities effectively burst through the Efficient Frontier and give you access to some risk-adjusted returns that investment professionals wish they could access.

FSCS savings protection

Before the FSCS was launched, consumers needed to carry out serious due diligence on their bank. After all, if the bank folded, the only group left holding the bag would be the depositors who placed their trust in the wrong institution.

But thanks to the FSCS, any FCA regulated bank that accepts deposits is effectively the same risk, whether they’re an old traditional bank, a brand new start-up, or even the subsidiary of a African bank. That risk is effectively zero risk, because the FSCS will reimburse you for any lost money in the event the bank becomes insolvent.

This means that consumers looking to save under the £85,000 limit should remove their filters and be prepared to bank with unusual brand names or foreign-sounding businesses if it means receiving a higher interest rate.

With risk at zero, a higher interest rate will always result in a higher risk-adjusted return, so it’s objectively the better investment.

Of course, this only applies if the bank truly is FCA regulated and covered by the FSCS so a minimum level of due diligence is still needed to ensure you’re not falling victim to a scam.

Employer pension contribution matching

All employers are required by law to match employee contributions into a workplace pension scheme up to 3% of pensionable pay.

This means that for every £1 you add into your pension pot, your employer will contribute a further £1. This is money that you would otherwise not receive, because un-used matching money cannot be paid out as part of the salary.

Employer matching effectively provides a 100% return on your pension investment on day one. This, in addition to the fact you can contribute gross salary to a pension scheme tax-free, makes this an incredibly profitable investment. On a risk-adjusted basis, it will exceeds the expected returns of any investment you could use your net pay for if you chose not to contribution to your pension.

How to manage the stress of risk

While we have already made clear that you should always invest within your comfort zone, here are some tips on how to expand the size of that comfort zone.

- Invest for the long term and never deviate from that long term strategy

- Invest on autopilot to remove decision-making from the process as much as possible

- Focus on the income generated by a portfolio rather than its capital value to keep track of the underlying growth in your investments even during turbulent periods

Our investing psychology series of articles dig much deeper into these tips and explain why each can be so powerful in conquering fears we sometimes have about investing.

These include How to deal with loss, how the income mindset could improve your risk tolerance, and how to invest on autopilot.

I hope you’ve enjoyed this comprehensive guide to investment risk.