Retiring early is the well-deserved reward for a period of incredible effort. Whether we enjoy our work or dread the beginning of each week, most of us share a common goal to unlock unlimited free time and wave goodbye to the pressures of employment. This is our guide to how to retire early.

Of course, almost all of us will retire eventually. But whether we retire early enough, or with enough pension provision to allow us to lead the lifestyle we would want… that’s all to play for.

Retirement planning is like building the house of your dreams

Preparing for retirement is like building a holiday home throughout your working life. Given that we’re dreaming here, why not visualise your holiday home as a beautiful villa on the beachfront.

As you save money through the years, bit by bit, you will assemble pieces of this property until it can stand alone and support you independently.

Once the final touches have been added, you are free to untether yourself from a wage or salary and enjoy the fruits of your labour over the years.

Every working adult is doing this to some extent, some more productively than others. In practice, many Brits run out of time. They’ve got strong foundations but had to cut corners on the flooring and walls, and didn’t have time to add the roof!

In this article, we’ll explain the vital components of this project and what you should be doing and when to retire early on your own terms.

How to retire early: at a glance

Your retirement holiday home has the following components:

- Foundation – becoming debt-free

- Floor – growing your net worth

- Walls – building a passive income

- Roof – securing financial protection

Let’s look at these in turn.

1. Becoming debt-free for early retirement

It isn’t difficult to understand why debt is enemy number #1 for most retirement planning books:

- Our over-arching objective of saving for retirement is to accumulate so much in assets that we are able to live off them until our final day.

- But debt is the opposite of wealth. Rather than providing us with interest income or capital that we can withdraw, debt is a drain upon our financial position.

Credit cards and personal loans don’t only incur an interest cost each year, but if left unchecked, they can continue to grow.

Just like a cancerous tumour placing the rest of the body at risk; debt brings a threat of consuming an ever-greater portion of your savings and investments.

Tips for paying down debt for retirement:

1. Focus on the debt with the highest interest rate first.

If you cannot pay down your borrowings in one go with spare savings, then it’s time to apply some strategy in deciding in which order the debts should be tackled.

Common sense dictates that you should pay down the debt with the highest interest rate. This way, you’re making your money save you the maximum interest possible by getting rid of the most ‘expensive’ debt. This will, in turn, provide you with more financial firepower over time to address other balances.

2. Restructure your loans before you pay them down

That being said, don’t assume that the interest rates on your debt are permanent. Credit card debt can be transferred to another provider, at which point you may be able to secure a 0% APR period. If this is the case, take full advantage of these offers and then tackle only the most expensive debt after you have restructured.

3. Use the tax-free lump sum from your pension scheme

If you have a defined contribution pension scheme, and still have remaining debts at the age of 57, HMRC provides you with a one-off opportunity to make that debt go away.

Upon retirement, you may withdraw up to 25% of the value of a defined contribution pension scheme completely tax-free. Many early retirees make full use of this allowance to pay off the remainder of their mortgage and tidy up any remaining debts.

We suggest you read the best books about getting out of debt for more inspiration.

2. Growing your net worth for early retirement

Now we’ve reached the main event, growing your net worth.

Your net worth comprises all of the things you own, less all of the things you owe. It represents your wealth and is the single biggest metric to monitor when planning for retirement.

Like a squirrel storing nuts, it’s obvious that the more money we tuck away, the more winters we’ll be able to survive off our own assets rather than needing to work.

As soon as you reach the magic figure for your lifestyle, you’ll be able to retire early.

How to calculate your magic number

To calculate your target wealth for early retirement, use this simple bit of maths:

Your target pre-tax retirement income / 0.04

For example, if you would like to receive £25,000 of retirement income, you would need to calculate £25,000 / 0.04 = £625,000 of net assets, which you can use a pension calculator to calculate.

This is a simplistic calculation because it assumes that you will need to rely upon your own assets for all of your income. In reality, you will become entitled to state pension at 65, may have other pension provision (such as a defined benefit scheme), or might qualify for other state benefits.

However, you can take the magic number as a conservative estimate for the amount of wealth you need to retire early, kick back and take it easy.

How to accelerate your net worth

Once you understand your retirement wealth target, your focus can now shift to getting there as quickly as possible.

If you need to reach £625,000 and you currently have a net worth of £225,000 then this gives a £400,000 shortfall to fund.

You could simply take this gap and divide it by the number of years until your ideal retirement date, and this would give you a fixed sum you need to save each year to hit your goal.

However, if your retirement date is more than 10 years away then you should be able to reach it much faster if you saved that annual amount. That’s thanks to the compounding returns on your existing savings and investments.

The best investment for early retirement seekers is equities, because they offer a high return over long periods of time. Buying shares for a short term savings goal is risky, but over decades equities is a very reliable asset class and regular beats all other assets, such as property, cash and bonds over these long periods.

Mastering your saving ratio

The largest factor in allowing you to retire at 50 or earlier is your saving ratio. This is the relationship between how much you save and how much you spend each month.

Someone who lives at their parents and doesn’t spend a penny has a saving ratio of 100%. Someone who lives at the edge of their means and runs out of money at the end of each month has a saving ratio of 0%.

Financial advisers generally suggest that we aim to save 20% of our post-tax income each month over the course of our lives to fund a reasonable retirement. This is only a rule of thumb, as other decisions such the risk level of your retirement investment portfolio will also greatly impact whether you’ll be able to get rich quick.

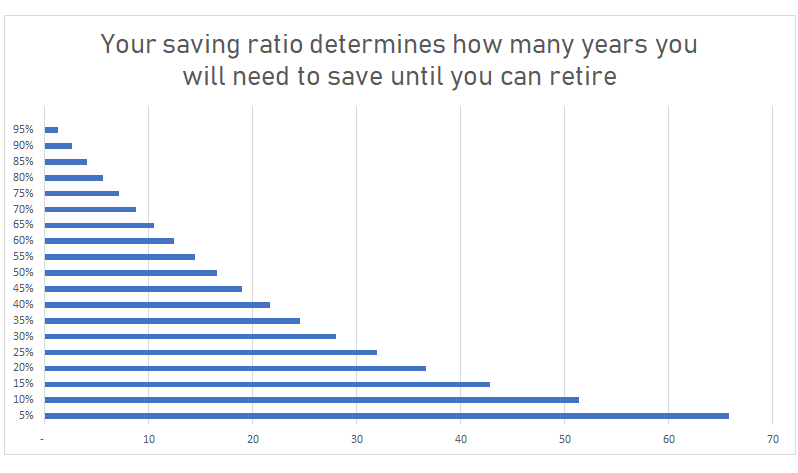

We’ve produced a chart below to show how the number of years until you can retire is very dependent on your saving ratio.

The saving ratio has such an extreme effect because increasing your saving rate helps in two ways:

- It adds more money into your net worth

- It implies you’re spending less, therefore your target income (and therefore target net worth) falls.

Said in another way, the more you save, the less you spend. The less you spend, the lower your income needs will be in retirement. The lower your income needs, the lower the target net worth to be able to retire early.

The secret to early retirement is not about maximizing your earnings – it’s minimising your spending too. If you can find cheaper ways to live your life, you could cut 10 or even 20 years off your retirement date.

Just look at the difference between career length for someone who saves 10% of their income (51 years) and someone who saves 30% (28 years). That 20% could be simply the choice to not move into a large home at middle age. And with that single decision, you could unlock two decades of free time to learn to love your existing home and garden.

Chart’s like these are powerful because they force us to trade off time and money in ways that we never have the time to do at the cash register.

3. Building a passive income for early retirement

Once you have built a net worth which allows you to retire, what do you do with it? Do you just keep your investments as they are, or do you redesign your portfolio for retirement?

The answer will depend upon what types of accounts you hold your wealth in. Are they pension schemes, stocks & shares ISAs or standard stockbroker accounts?

Is any of your wealth a family business or perhaps did you use one of the best crowdfunding sites (such as Funderbeam) to buy small shareholdings in private high growth businesses?

The different way in which investments are taxed or liquidity restrictions may make this a complex decision. You can seek help from a financial adviser to assess your needs and recommend an investment plan for your new life.

If you have a fairly simple portfolio, the key change you need to make it to de-risk enough assets to ensure that you can cover your living expenses (plus some unforeseen ones) for the next 10 – 15 years. The remainder of your assets can be invested (subject to your personal risk appetite) for the greatest return.

You’ll have to continue to reassess this risk v liquidity relationship each year to ensure that you:

- Don’t run out of cash or are forced to sell shares at short notice

- Are putting surplus funds to work as hard as possible.

In our guide on how to invest your money, we reiterate that you shouldn’t invest money in shares if you need to access it in under 10 years. This is a golden rule of retirement investing, and is why should always have a portion of your portfolio clearly ringfenced as being short term, which can be invested in bonds or savings accounts.

Retirement investors who want to take more risks take an alternative route of investing most of their assets into income-producing financial instruments such as dividend shares, preference shares, the best funds that invest in bonds, and Real Estate Investment Trusts.

This way, they maximise the total income yield of their portfolio and live off these income streams as a primary source of income.

This is not financial advice – please seek help from a financial adviser if you are unclear about your options or aren’t sure which strategy is the most appropriate in your personal situation.

4. Securing financial protection for early retirement

Finally, when learning how to retire early, you should consider whether you have insurance needs.

By leaving the labour force at a younger age, you may still have children, mortgage payments and other obligations that a 68-year-old may not have. In other words, retiring might be more complicated.

Insurance policies can help to protect your family. For example, life insurance is a cheap way to ensure that if one parent dies, the other will be able to immediately settle any debts and pay off the house.